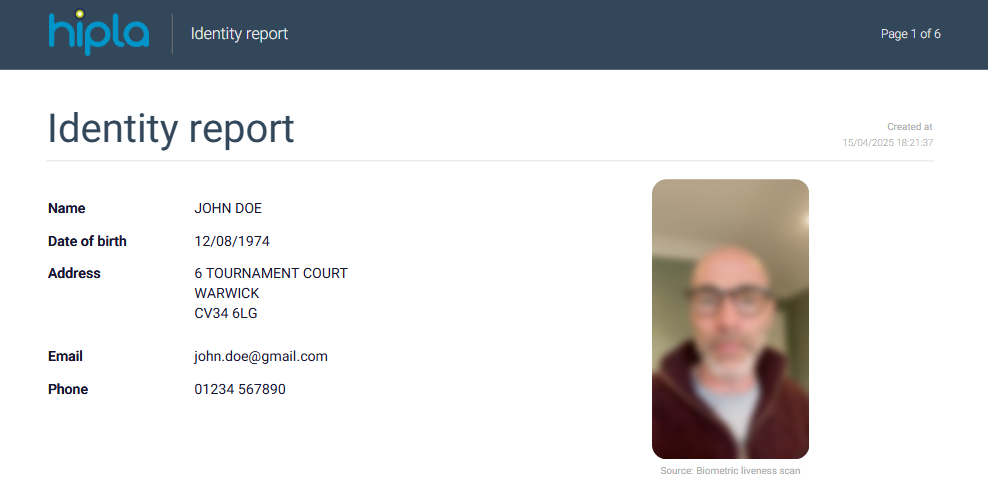

For a check that your client has completed (such as a Full Biometric check) the first thing to review are the client details (name etc) and biometric image of them to ensure that it is the person who you expect (based on the information you already have) and that there is nothing unexpected. An incorrect name will mean that AML has been run on an incorrect subject.

The next part of the report details the type of check that has been completed and this should be appropriate for your business case:

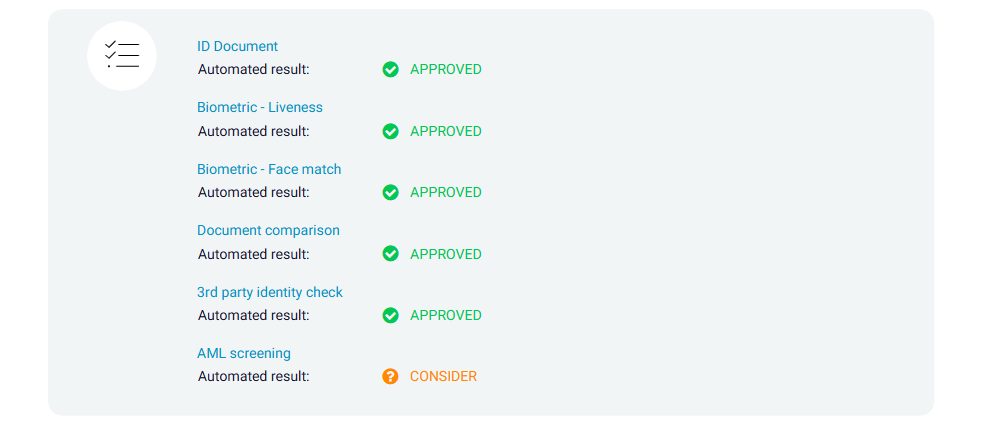

The rest of the front page then provides a high level summary of the initial results of each of the subjects that are included in the specific check type:

A green tick with the word ‘APPROVED’ means this section of the check has passed:

ID document - The ID document presented is genuine and valid.

Biometric liveness - The biometric scan determined that the person was present and not someone wearing a mask or presenting a video to camera of a person from whom they have stolen a genuine identity document.

Biometric facematch - The face presented during the face scan matches that on the ID document.

Document comparison - The names on the address document match those on the ID document.

3rd party identity check - A match has been found for this identity with a 3rd party Credit Reference Agency. It is much harder to fake an identity through time than it is for a single moment in time.

AML screening - No potential matches have been found when searching hundreds of different AML data sources.

If something is flagged as ‘CONSIDER’ or ‘REJECTED’, it doesn’t mean to say that you can’t do business with your client. You will need to review the specific results presented and make a determination based on all the information being presented to you in conjunction with your own internal AML compliance policy. Sub checks can be flagged as ‘CONSIDER’ or ‘REJECTED’ for multiple different reasons, for example:

The names on the address document and ID document may not have had an exact match, for example dual names versus individual name.

An imprint of someone may not have been found at the Credit Reference Agency and there can be multiple different reasons why.

The AI may not have been categorically able to rule out that it wasn’t a video being presented to screen instead of a real person during the facematch scan etc..

A potential match may have been found on one of the AML databases because people share names and date’s of birth.

To record your decision making process we recommend you update the ‘OUTCOME’ of the individual sub check. To do this just review the report and click on the ‘UPDATE OUTCOME’ button at the bottom of the screen:

Our compliance approval workflow will guide you through each sub check that may need your attention, providing you guidance on what to do and enabling you to record your decision making process. Once done, the PDF report will reload, your commentary will be recorded and the indisputable timestamped audit history for the report will be updated. We then recommend you download and save this updated version.

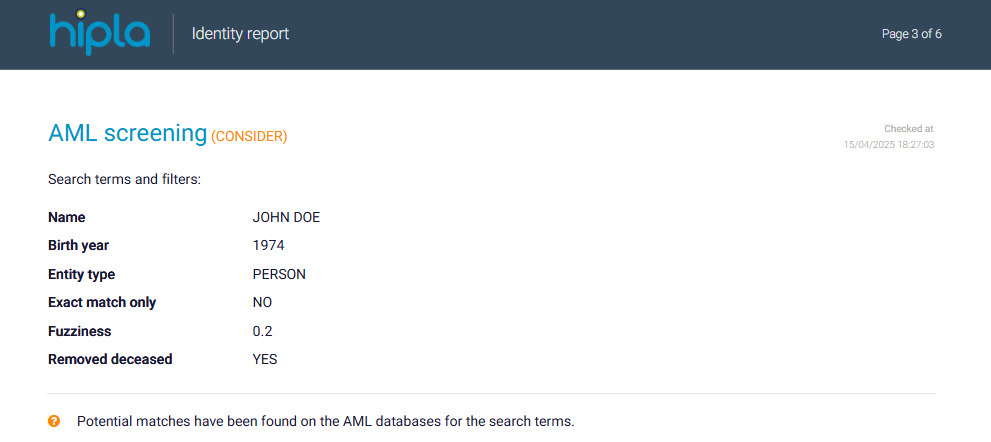

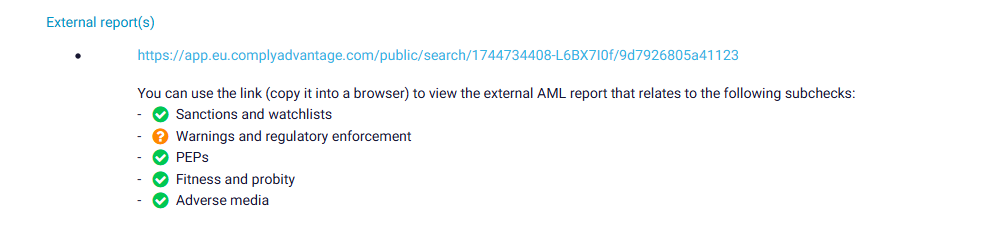

As you know, AML is checked against up to 5 different AML categories:

Sanctions and watchlists

PEPs

Warnings and regulatory enforcement

Fitness and probity

Adverse media

You will see the search criteria used for the check within the report:

People share names, date’s of birth and additionally it is common practice with AML to apply a level of fuzzy logic for name matching. This fuzzy logic can increase the number of false positives and as such we provide the ability for our clients to set this to a level of their choosing.

To review the list of potential AML matches just click on the link in the report which will take you through to the ComplyAdvantage portal:

We recommend you approach potential matches in the following manner:

a) Firstly, see if any potential match relates to your client or not. You can do this by checking that the search criteria was correct and reviewing the information returned in each search result. Data is sourced from thousands of different databases and each maintains a different level of information, for example sometimes a DOB is available, sometimes just a year a birth and sometimes neither. We show as much information as is made available to us.

b) If you think a potential match does relate to your client, then does it prevent you doing business with them? i.e. is it a sanction. If it is your client and they are sanctioned then you can’t do business with them and must report this.

c) If it doesn't prevent you doing business with them then does it elevate the risk of doing business with them? For example if a PEP is returned it doesn't prevent you doing business but it does elevate the risk of money laundering due to position of office, risk of blackmail, potential of abuse of position etc. so depending on the activity you may choose to accept/acknowledge the risk but perform a higher level of client due diligence and potentially be looking out for other red flags on the transaction etc.

If you're unsure or need individual compliance advice then we recommend taking this up with your internal (or external) compliance officer.